How Does The Affordable Care Act and ObamaCare Affect My Taxes?

Just like most IRS and government agency questions, the tax consequences of the Affordable Care Act differ from person to person. The greatest change has been for Americans who purchased insurance through the Individual State Exchanges on HealthCare.gov. Taxpayers with no insurance see the next greatest difference, followed by those with insurance through their employer or as a government benefit.

Let’s take a look at a short summary of each classification. This information should encompass most people, but there will always be exceptions.

HealthCare.org Purchasers

Similar to when you take on any insurance policy, it comes with several pages of rules, exemptions, exclusions, rules, and expectations. No surprise to many that the new requirement of the Form 1095-A when filing the 2014 Federal Tax Return has been missed or forgotten by the unsuspecting masses.

What is the 1095-A Form? It is similar to a W-2 for work. The document is the year-end statement that the insurance provider sends to the IRS that the taxpayer must include in their paperwork.

How does the 1095-A Form affect your refund? The purpose is to compare or “true up” how much government subsidy you should have received when purchasing your insurance.

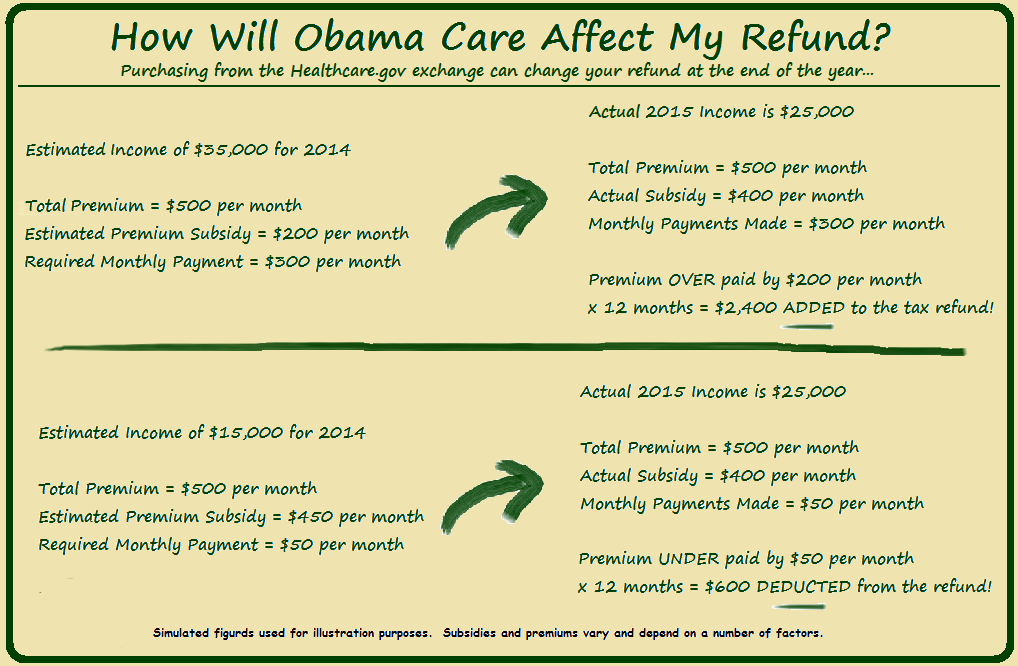

Upon signing up, you are asked to estimate your future income for the year. This is used to establish how much of your total insurance premium is to be paid via government subsidy and how much is to be paid by you.

The following year in late January or early February, the 1095-A is issued by the Exchange to see how much subsidy you were actually entitled to receive. If you overpaid the premium, you get a larger tax refund. If you were given too much subsidy, the excess of the subsidy is subtracted from your tax refund.

DO NOT FILE YOUR TAXES WITHOUT THE 1095-A FORM!

This can be worse than leaving out a W-2. The primary difference is that the IRS will simply refuse to pay your refund until you update the return if you forget the 1095-A. If you forget a W-2, the IRS will pay out the original refund and expect you to fix it later, regardless of whether or not you owe more back or get an additional refund.

The Uninsured

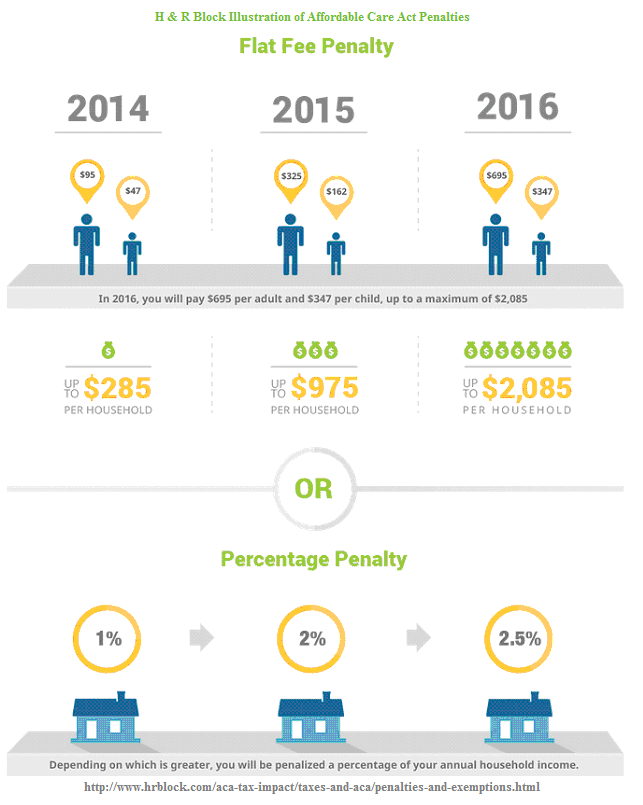

The affects of the Affordable Care Act on the uninsured are more straight forward, depending on your income level. Most are required to pay a penalty of $95 per uninsured adult or 1% of their annual income, whichever is greater. An additional penalty of $47 applies for each child dependent without health coverage in 2014.

These penalties are expected to more than double in 2015 and increase again in 2016.

For some people, IRS regulations provide a number of hardship exemptions that waives the fines for not having health coverage. These range from low income hardships to religious reasons for not being covered, Native American tribal membership, just to name a few.

The definition of ‘low income’ for the affordability hardship varies for different situations.

Go to http://www.healthcare.gov/fees-exemptions/exemptions-from-the-fee/#hardshipexemptions for more information on exemptions.

How do the Affordable Care Act fines affect your refund? Very simple. If you do not qualify for a hardship exemption, the penalty is deducted from your refund, much like an additional tax.

If you are procrastinating about signing up for health coverage, the following illustration from http://www.HRBlock.com provides a breakdown of the current and future penalties for not having health coverage.

Insured Via Employer, Medicare, Medicaid, or Other Source

Good news! For Americans insured by their employer, covered by Medicare, Medicaid, COBRA, Veterans Affairs, or any other state or federal benefit, your tax preparer will simply answer a question in their accounting software to eliminate any penalties. Obama Care is just that simple.

If you are insured through your employer, the information is included on your W-2 Form. Normally the health coverage is included in Box 12 next to the “DD” classification code. The IRS will get this information when your employer reports their W-2 Forms later in the year.

What if I am preparing my own personal tax return? Check the “Full-year coverage” box on Form 1040 in line 61, on Form 1040A in line 38, or on Form 1040EZ in line 11.

The Takeaway

Remember, this was year 1 for Americans having to include health coverage on their tax returns. It takes a few years for everyone to fully understand what is required on the IRS Form 1040. Education takes time.

Many people did not realize that the 1095-A was even coming. Now their tax refunds are delayed by several weeks.

Although the 1095-A Form process was disclosed upon signing up on HealthCare.gov, the education of the public was lacking, at best. How often do your read EVERYTHING when signing up for a new insurance policy, credit card, or savings account?

Barring other issues with the IRS or Congressional disputes, things should be smoother next year.